Air Doctor provided The Phoenix with a global medical network through which its travel insurance customers could access outpatient medical care abroad at no cost to them

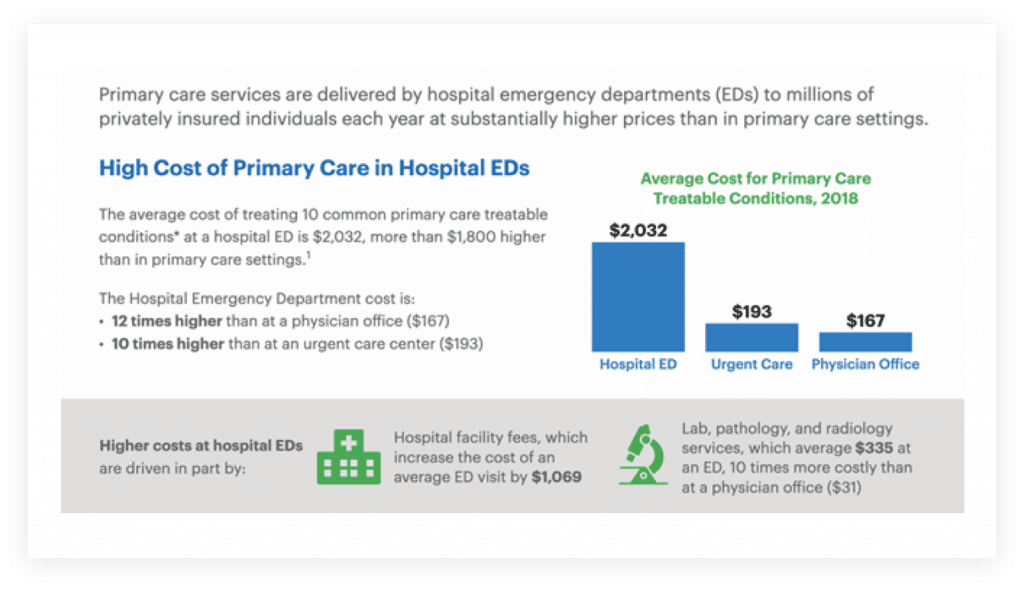

The primary aim was to reduce reimbursement costs for The Phoenix by preventing expensive and often unnecessary inpatient stays at (emergency) care facilities

The secondary aim was to improve the experience for travellers by enabling them to search for doctors by proximity, medical specialism, and languages spoken, among other factors, in order to directly reach the most appropriate care

Air Doctor redirected 15 per cent of inpatient hospital visits to outpatient settings

The Phoenix recorded that 5 per cent of claims would have required hospitalisation without Air Doctor, resulting in an average cost of $2,660 per claim

Use of Air Doctor reduced the average outpatient claim from $171 to $150, including Air Doctor’s commission which was taken from the doctor’s fees at no cost to The Phoenix

By centralising invoicing and automating their processing, Air Doctor also managed to streamline payments for The Phoenix, reducing time spent on administrative tasks and, consequently, back office costs

Overall, there was a 14% reduction in outpatient to outpatient costs, saving over $1 million for The Phoenix and a 30% year-on-year policies increase which boosted The Phoenix’s market share

The total sample size was one million policies sold